Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam nonumy eirmod.

Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam nonumy eirmod.

Alex

Jun 12, 2026

The model is simpler than most people expect. You charge a service fee on every ticket sold, a buyer pays the total price, and you keep the difference between the fee collected and the cost of running the transaction.

That difference is smaller than the headline number suggests.

Here is the standard structure. A ticketing platform charges 10% on a $50 ticket, generating $5 in gross revenue per ticket. Stripe then takes 2.9% of the full charge plus $0.30 per transaction. On a $50 ticket that is $1.75. You are now at $3.25 net before venue costs, platform infrastructure, or customer support.

Multiply that by volume and you have a business. The model works because fixed costs do not scale linearly with ticket volume. An operator processing 500,000 tickets per year spreads the same engineering and compliance overheads across a base ten times larger than one processing 50,000. Margin per ticket improves steadily with volume, which is why this business rewards growth more than almost any other.

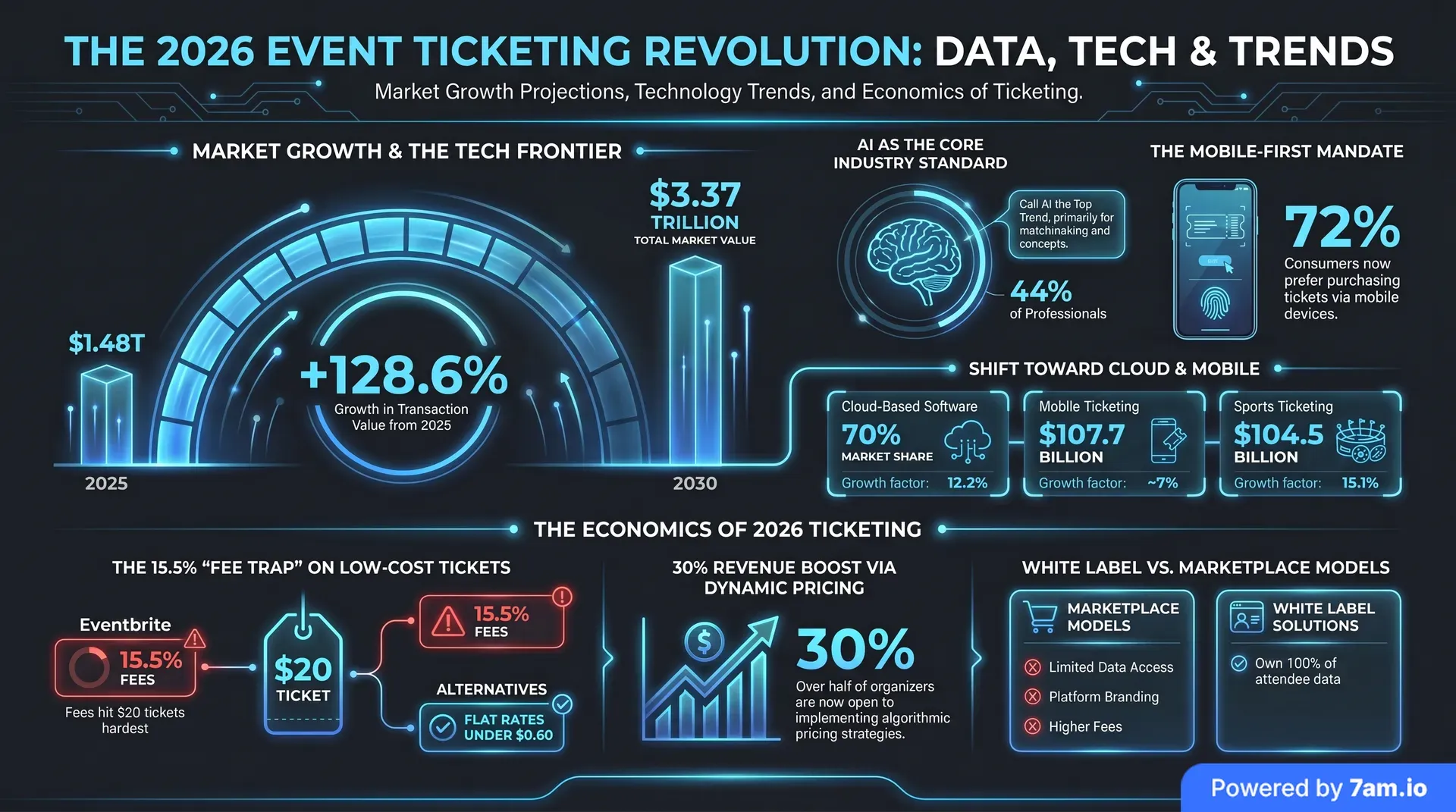

The market they operate in is large and expanding. The total ticketing transaction market sat at $1.47 trillion in 2025 and is projected to reach $3.37 trillion by 2030, a 128.6% increase in five years. Music and festivals account for 27% of transactions, sports for 32%, and mobile devices now process 59% of all ticket purchases. The ceiling is not a constraint right now. The floor is building enough volume to cover fixed costs.

The range is wide, and the effective rate matters more than the headline percentage.

Eventbrite's Flex plan charges 3.7% plus $1.79 per ticket, plus a separate 2.9% payment processing fee per order. On a $20 ticket, the total fee reaches $3.11, an effective rate of 15.5%, more than three times the headline percentage. TicketSpice charges a flat $0.99 plus 2.9% plus $0.30 per transaction, roughly $2.74 on a $50 ticket. Ticket Tailor charges $0.22 to $0.60 flat with no percentage component.

At the top of the range: Ticketmaster. Service fees on major general admission shows run 27 to 31% of the face value. That figure, highlighted in US Senate hearings and FTC investigations since 2023, is not a total-including-processing number. It is the service fee alone, on top of the base ticket price. The company generated over $22 billion in revenue in 2023 on roughly $36 billion in gross transaction value.

That last figure is worth sitting with. Ticketmaster captured around 61 cents of every dollar flowing through its system in 2023. That is revenue, not margin, because what the headline number hides is the venue rebate structure.

Venues with meaningful foot traffic charge ticketing companies for exclusivity. That cost comes in three forms: upfront key money payments (ranging from thousands to hundreds of thousands of dollars at major venues), per-ticket rebates, or a share of total service fee income. The share model is the most common at scale, and the numbers are significant: rebates to venues typically represent 40% to 60% of the total ticketing fees charged to buyers. A 10% service fee becomes an effective 4% to 6% before any other line item.

This is the cost that how organisers think about ticketing fees eating their own profits rarely makes visible, because from the organiser's view, the platform is the one charging. From the platform's view, the venue is the one collecting.

Payment processing is the most visible variable cost, but it is not the largest.

On a batch of 10,000 tickets at an average price of $60, Stripe takes roughly $17,400 in processing fees. Service fee at 8% on those tickets is $48,000. Before everything else, the spread is $30,600.

Everything else is the problem.

A self-built platform carrying meaningful volume needs at minimum two senior backend engineers at $180,000 to $240,000 per year in NZ or Australian salaries, before benefits. Hosting costs scale sharply during onsale traffic spikes. PCI-DSS Level 1 compliance audits run $50,000 to $300,000 per year at high transaction volumes, and the audit is an annual recurring cost, not a one-time gateway. Then there is customer support: buyers contact the platform about missed confirmation emails, refund requests, name-change queries, and door scanning failures. Every chargeback costs the platform $15 to $35 in dispute fees, and the chargeback rate on ticketed events typically runs 0.5% to 1% of transactions.

The industry benchmark for a new self-built platform in 2026 is a minimum cash buffer of $196,000 to cover development and the operational ramp-up period, with break-even typically arriving around 18 months after launch. That timeline assumes things go reasonably well.

A white-label operation built on an existing platform cuts most of this out. The platform provider carries PCI compliance, engineering, and onsale infrastructure. Your cost structure compresses to: the platform fee on each ticket, your organiser acquisition costs, and whatever support capacity you provide for organiser relationships. Processing costs stay, but someone else orchestrates the compliance around them.

The decision between these two paths is covered in depth in the build vs buy breakdown. The short version is that white-label is almost always right for a new entrant, and building only makes sense when ticketing technology is the product you are selling, not just the road buyers walk to reach your product.

This is the number most ticketing business plans get wrong, and it changes everything about the model.

Acquiring an event organiser costs around $300 in customer acquisition cost. Acquiring a ticket buyer costs around $15. The ratio is 20:1.

That asymmetry has a direct implication: the business only works if organisers stick. One organiser running 12 events per year at 800 average attendance generates roughly 9,600 tickets annually. At $3 net per ticket, that is $28,800 per year from a single relationship, without additional acquisition cost. Lose that organiser and you spent $300 to acquire them plus $28,800 in future annual revenue. Replace them with a new organiser and spend another $300. The compounding cost of churn is brutal.

This is why the ticketing companies that survive, not just the ones that launch, are the ones that become genuinely valuable to organisers, not just transactionally convenient. A platform that helps an organiser run better events, sell more tickets, and understand their audience data becomes hard to leave. A platform that is just slightly cheaper than Eventbrite is not.

Understanding why attendee data is more valuable than the lineup is the organiser argument a white-label ticketing company can make that no marketplace can match: on our platform, you own every contact. On Eventbrite or Ticketmaster, the platform co-owns the buyer relationship and can market competitor events to your audience.

Break-even is a function of fixed-cost absorption, not fee percentage.

A self-built platform with two engineers and a compliance bill carries roughly $400,000 to $600,000 in fixed annual costs. At $3.25 net margin per ticket after processing (on a $50 ticket at 10%), that requires 123,000 to 185,000 tickets per year just to cover fixed costs, before sales, marketing, and support.

A white-label operator on an established platform has a fundamentally different cost structure. Absent build costs, engineering, and compliance, fixed overheads might run $80,000 to $150,000 per year. At $2.25 net margin per ticket (10% service fee, minus 5% platform fee, minus processing), break-even lands at 35,000 to 67,000 tickets per year. A regional operator with ten organisers each running three events per year at 500 average attendance reaches that on 15,000 tickets per year, well short of break-even, but closer than a self-built platform would be at the same stage.

A single mid-size festival with 8,000 capacity and two events per year gets you to 16,000 tickets. Two of those and you're profitable.

At 500,000 tickets per year, the economics look like this:

| Line | Amount |

|---|---|

| Gross service fee revenue (7% net) | $1,750,000 |

| Processing costs (2.9% + $0.30 avg on $60 tickets) | ($105,000) |

| Platform/infrastructure fees | ($120,000) |

| Venue rebates (~30% of gross at this volume) | ($525,000) |

| Support and operations | ($180,000) |

| Operating profit | $820,000 |

That is a 46.9% operating margin at meaningful scale. Getting there from zero is the hard part, and choosing the right ticketing system infrastructure early determines whether you are building toward that margin or fighting it.

Not per-ticket fees. Organiser relationships and subscription density.

Commission income accounts for around 70% of revenue at most established ticketing platforms. It is also lumpy: it follows event calendars, peaks in summer and around major holidays, and craters in January. The operators that survive bad quarters are the ones that have built a subscription revenue layer on top.

Premium subscription tiers, charging major promoters $7,500 per month for advanced analytics, marketing tools, priority onboarding, and dedicated support, provide the predictable cash flow that commission income cannot. A platform with 20 major promoters on $7,500/month subscriptions has $1.8 million in recurring annual revenue before a single ticket is sold. That is not hypothetical: it is a documented structure among mid-tier platforms competing below Ticketmaster.

The other margin driver is switching cost. An organiser who has run 50 events through your platform has years of historical sales data, audience records, and event templates on your system. Switching platforms means migrating that history, retraining their team, and rebuilding their audience segment lists. Switching cost compounds with tenure, which is why acquisition-to-event-one is worth significantly less than acquisition-to-year-three.

For a white-label operator, the equivalent of venue rebates is the platform revenue share. That is the slice the underlying platform takes on each transaction. On 7am's model, where the booking fee starts from 5% and you choose whether to charge 8% (keeping 3%), that spread is your gross margin before processing. As volume grows and you add subscription tiers on top, the margin profile looks significantly better than commission alone.

The ticketing mistakes that cost operators real money are rarely on the fee side. They are on the retention side. Organisers who leave after two events cost far more than a basis point of margin.

The unit economics of a ticketing company work when two things are true: organiser acquisition cost is recovered quickly through volume, and organiser relationships are retained long enough for the recurring margin to compound.

The fee structure is the entry point, not the moat. Every competitor can match your percentage. What cannot be matched overnight is a platform where organisers have history, audiences have accounts, and the switching cost is real.

White-label on 7am's rails gets a new operator to their first organiser in weeks instead of months, with a cost base shaped for the early volumes a new entrant can realistically sign. The margin profile at year one is thin. At year three, with organiser retention and a subscription layer building, it is a real business.

The dynamics of how platforms handle slow payouts and organiser trust are worth understanding before you set your payout policy. Getting it wrong is one of the fastest ways to lose an organiser you just paid $300 to acquire.

Explore More

View All