Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam nonumy eirmod.

Lorem ipsum dolor sit amet, consetetur sadipscing elitr, sed diam nonumy eirmod.

Charlie

Jun 5, 2026

Buy Now, Pay Later (BNPL) lets a buyer split a ticket into instalments, usually four payments over six weeks, while you, the organiser, get the full ticket price up front. A provider like Afterpay, Klarna, or Affirm pays you in one lump and collects the instalments from the buyer themselves.

That last part is the bit most organisers get wrong. They assume "payment plan" means they're waiting around for four dribbles of cash. They're not. The buyer pays over time. You get paid now, minus a fee. The provider carries the gap.

It's the same mechanic that's been sitting on Coachella and Glastonbury checkouts for years, now showing up on regional festival and venue carts. A punter who couldn't drop $240 in one hit can commit to $60 today and three more $60s. The sale closes instead of getting abandoned in a browser tab.

Yes. With the standard "Pay in 4" model, the BNPL provider settles the full ticket price to you within a day or two of the sale. Same as a card payment, just routed through Afterpay or Klarna instead of Visa.

Here's why that matters. The buyer might miss their third instalment in five weeks. That's the provider's problem, not yours. Afterpay and Klarna underwrite the repayment risk, so if the buyer defaults, the provider eats it. You've already banked the money and printed the ticket.

This is the opposite of laypay or "hold a spot" schemes some organisers cobble together, where the attendee pays you directly in chunks and you're exposed if they ghost the last payment. Real BNPL moves that risk off your books entirely. If you've ever stressed about how fast ticket money actually lands in your account, BNPL doesn't slow you down. Settlement timing tracks your normal payout schedule.

The one wrinkle: chargebacks and disputes still route through the provider's process, which is its own animal. More on that below.

BNPL costs you a merchant fee of roughly 3% to 6% per transaction, higher than the 2% to 3% you'd pay on a standard card. The buyer pays nothing extra if they keep to the schedule. The provider makes its margin from your fee plus any late fees the buyer triggers.

So a $200 festival ticket sold through Afterpay might cost you $8 to $12 in fees versus $5 on a card. That's $3 to $7 of margin gone per ticket. On 3,000 tickets, the gap is real money.

The question isn't whether BNPL costs more. It always does. The question is whether the extra sales it opens up outrun the extra fee. If turning BNPL on lifts your conversion by even 5%, the maths usually wins, because the incremental tickets were sales you'd otherwise never have made. This is the same logic behind why discounting isn't the only lever for lifting conversions. You're removing a price barrier without cutting the headline price.

Run the number against your real margin before you switch it on. If you're already operating on thin ticket margins, that 3-point fee gap can be the difference between a profitable show and a break-even one. Organisers who track profitability per ticket properly tend to make this call in about thirty seconds.

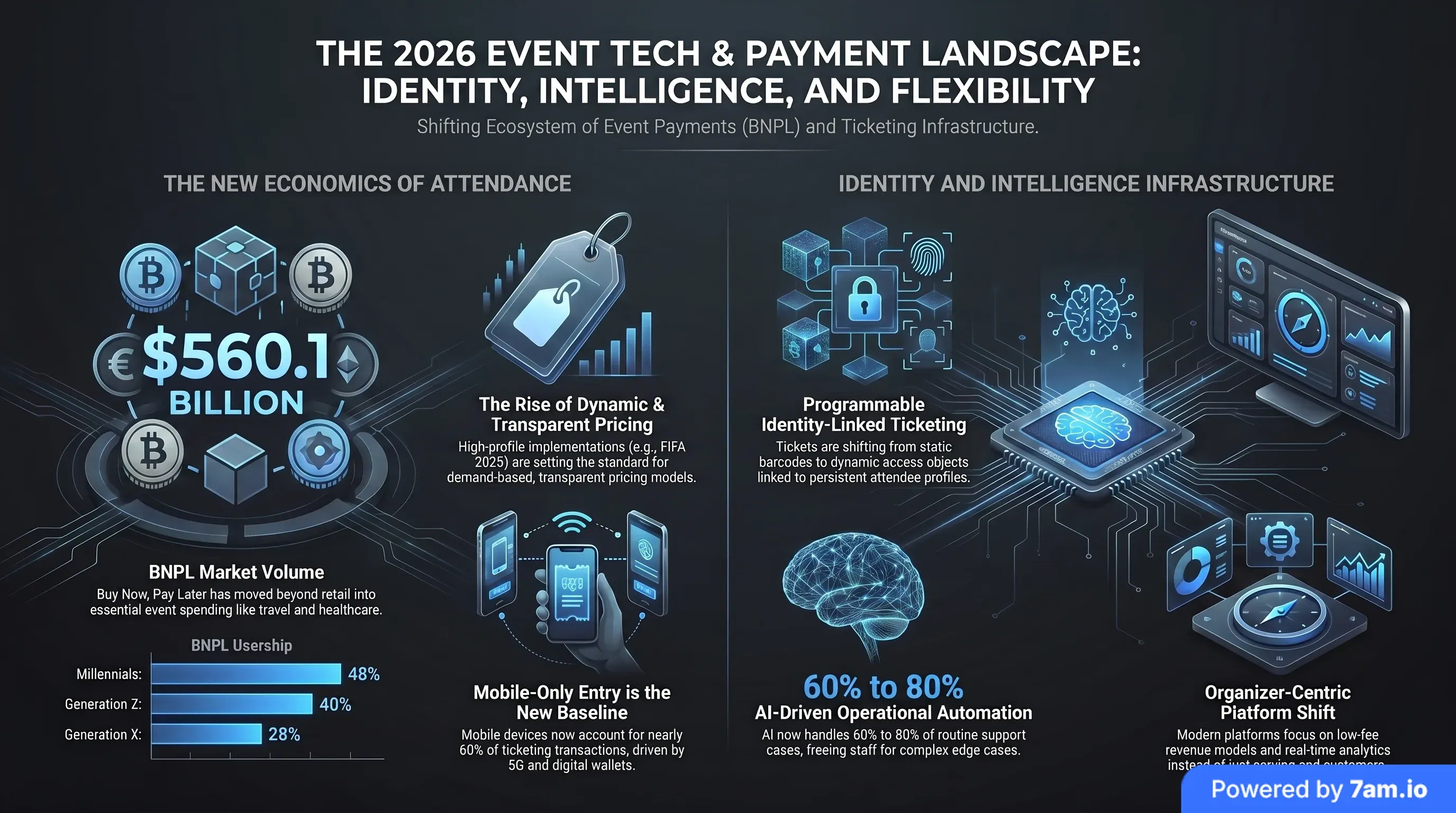

The hard evidence says yes, especially for younger audiences and higher-priced tickets. About 60% of general-admission buyers for Coachella in April 2025 used the festival's BNPL payment plan. Sixty percent. That's not a fringe feature. For a young festival crowd, instalments are the default way to buy.

The behaviour underneath it is well documented. 44% of Gen Z used BNPL in 2024, and over half of Gen Z and Millennials reach for it ahead of a credit card. These are the same buyers who wait until the last week to commit and who care more about the vibe than the production budget. Cash flow, not desire, is what stops them. BNPL removes the cash-flow wall.

BNPL also nudges average order value up. Across merchants, instalment options lift average order value by 15% to 40%. A buyer staring at a $180 GA ticket might trade up to the $260 VIP when the number they see at checkout is "$65 today." The total feels smaller even though it isn't. Organisers running tiered upgrades and add-ons see this lift most clearly.

There's a softer benefit too. A ticket abandoned at the payment step is a near-miss you usually never recover. Treating checkout abandonment as the revenue leak it is means giving the hesitant buyer one more way to say yes. For a chunk of your audience, that way is instalments.

Four providers handle most event ticket volume: Afterpay, Klarna, Affirm, and PayPal's Pay-in-4. Zip and Sezzle round out the field. They differ on instalment structure, market reach, and the ticket price range they suit.

| Provider | Instalment structure | Merchant fee | Who carries default risk | Key markets |

|---|---|---|---|---|

| Afterpay | Pay-in-4, interest-free over 6 weeks | 2% to 8% | Provider (Afterpay / Block) | Australia, New Zealand, US |

| Klarna | Pay-in-4, Pay-in-3, Pay-in-30, or longer financing | 4% to 6% | Provider (Klarna), pays you up front | US, Germany, Europe |

| Affirm | Pay-in-4 plus longer interest-bearing terms | 4% to 6% | Provider (Affirm), AI underwriting | US, larger and longer purchases |

| PayPal Pay-in-4 | Pay-in-4, interest-free | 4% to 6% | Provider (PayPal) | Global, 400M+ users |

| Zip | Pay-in-4 split-pay, interest-free | 4% to 6% | Provider (Zip) | Australia, US |

In every case the provider settles with you up front and carries the buyer's repayment risk. The merchant fee runs higher than card processing, and the structure shapes which ticket price it suits.

Afterpay pioneered the four-payments-over-six-weeks model and dominates events across Australia, New Zealand, and the US for mid-range tickets. Klarna offers more flexibility, with Pay in 3, Pay in 30 days, or longer financing, and has run direct promoter partnerships for festivals across Europe. Affirm leans toward larger amounts and longer terms, which fits multi-day passes and travel-inclusive packages. PayPal's Pay-in-4 piggybacks on the PayPal button a lot of carts already have, so it's often the lowest-friction one to switch on.

Which one you pick depends less on the brand and more on whether your ticketing platform already supports it natively. A provider you have to bolt on with custom code is a provider you won't maintain.

Offer BNPL when your tickets cost more than about $80, your audience skews under 35, or you sell multi-day and travel-inclusive packages. Skip it when tickets are cheap, margins are thin, or your crowd is older and corporate.

The price floor is the clearest rule. On a $25 community gig ticket, a 5% BNPL fee is $1.25, and the buyer doesn't need a payment plan for $25 anyway. The fee is pure cost with no conversion lift. On a $300 weekend pass, the same fee buys you a sale you'd probably lose otherwise. BNPL earns its keep as ticket prices climb.

Audience matters as much as price. A drum-and-bass festival in Tāmaki Makaurau with a 19-to-28 crowd will see BNPL adoption north of 40%. A $120 business breakfast for accountants will see close to zero, because that buyer expenses it on a corporate card and never thinks about instalments. Match the payment option to who's actually buying.

Margin is the veto. If you're running single-digit margins, model the fee against your real per-ticket economics before committing. BNPL that grows volume but turns a 4% margin into a 1% margin isn't a win. It's more work for less money.

The three real risks are brand perception, dispute handling, and tightening regulation. None are deal-breakers, but ignore them and they'll bite.

Brand perception is the quiet one. Putting "pay in instalments" next to a $400 ticket can read as encouraging young fans into debt for a weekend. Some organisers are fine with that. Some aren't. A youth-focused arts festival pulled BNPL off its student-priced tickets in 2025 precisely because the optics clashed with its values. Know where your line is before a journalist asks you about it.

Disputes are the operational one. When a buyer charges back a BNPL purchase, you're dealing with the provider's process, not your card processor's, and the rules differ. Build that into how you handle refunds and no-shows rather than discovering it during a messy weekend.

Regulation is the slow-moving one. The US CFPB and the UK FCA have both moved to treat BNPL more like credit, with affordability checks and clearer disclosure. The FCA begins formal oversight of the market in July 2026. That won't kill BNPL, but the terms providers offer you may shift. Don't build your whole pricing model assuming today's fee structure is permanent.

Protect your margin by passing the fee through, reserving BNPL for higher tiers, and using it to sell packages that wouldn't move otherwise. You don't have to absorb the cost on every ticket.

Passing the fee through is the bluntest fix. Surface it the way you'd surface any booking or service fee at checkout, and be transparent about it. A buyer who wants to split payments will usually accept a small premium for the privilege, the same way they accept the fee structures already baked into online ticketing.

Reserving BNPL for VIP, multi-day, and travel-inclusive tickets concentrates the fee where it does the most work. Those are the high-value purchases people most want to spread, and the margin on a $400 package absorbs a 5% fee far better than a $40 GA ticket does.

The trap to avoid is treating BNPL as a discount. It isn't one, and you shouldn't market it like a price drop the way some organisers market dynamic pricing and end up burning fan trust. BNPL is a flexibility feature. Frame it as "split your payment," not "save money," and you keep your pricing integrity while still catching the buyer who needed the option.

Buy Now, Pay Later pays you in full up front, moves the repayment risk to the provider, and costs you 3% to 6% per sale. For higher-priced tickets and younger crowds, the conversion lift usually clears that fee with room to spare. 60% of Coachella GA buyers chose it for a reason. For cheap tickets, thin margins, or older audiences, it's cost without payoff.

Run it against your own per-ticket margin, switch it on where the maths works, and pass the fee through on the tiers that can carry it. A ticketing platform that supports BNPL natively turns the whole decision into a toggle instead of a project, which is exactly how a payment option this proven should feel.

Explore More

View All